Writing Again, Without AI

March 2026 Update By David

At Abu Simbel during our trip to Egypt in March 2026.

The biggest change facing humanity is AI. There are many competitors for this nefarious title: national populism, religious extremism, climate change, wealth inequity, and nuclear war, to name a few. Admittedly, total annihilation is a non-zero chance. Short of that, AI technology will completely transform the modern human experience.

Predictions about AI are all speculative. AI is not known unknown—it is unknown unknown. The potential impact on markets and investments is staggering. I will share my thoughts on this more, but not in this note. I need more time to make it shorter (and not use AI).

A change at the firm

I haven’t written in a few years because Lifetime Financial has been busy, for which we are grateful. Growth continues non-stop thanks to your referrals and a good deal of organic interest after our website refresh. The reason I have time now is because I’m blessed to have the dynamic capability and steadfast leadership of Alishia Parkhill, my partner in business and life. She has skillfully transformed Lifetime Financial into a smoothly operating firm with much greater capacity than the sum of its parts.

Reflecting that, she’s taking over for me as the firm’s CEO and Principal, allowing me to remain focused on investment management, research, writing and client planning. As clients, you may have noticed a gentle shift over the last year. Other than that, you shouldn’t anticipate any change. This simply balances her title with her real contribution and aligns our respective roles.

Upcoming topics

Much has happened in the finance and investment world since I last chimed in. Trump savings accounts do not look great, but might be useful in some unusual circumstances. Home buying is finally loosening up as rates tick down and supply increases – but could be more expensive for a long time. There have been some not-insubstantial changes to charitable donation rules. There are new tax rates and rules, student loans are coming back online, and various other things are worth discussing.

But the top concern among clients is…politics.

What have the effects been of politics on markets?

It’s undeniably true that the Trump administration’s policies have increased uncertainty, something markets generally dislike. That uncertainty has increased volatility in stocks and bonds, including a drastic jump on ‘Liberation Day’ (April 2, 2025). Interestingly, swings one way or another have tended to calm down quickly, indicating a lack of confidence in Trump’s ability or willingness to carry out what he says he will do. Wall Street calls this the TACO-trade, or ‘Trump always chickens out’.

Inflation, bubbles and concentration risk

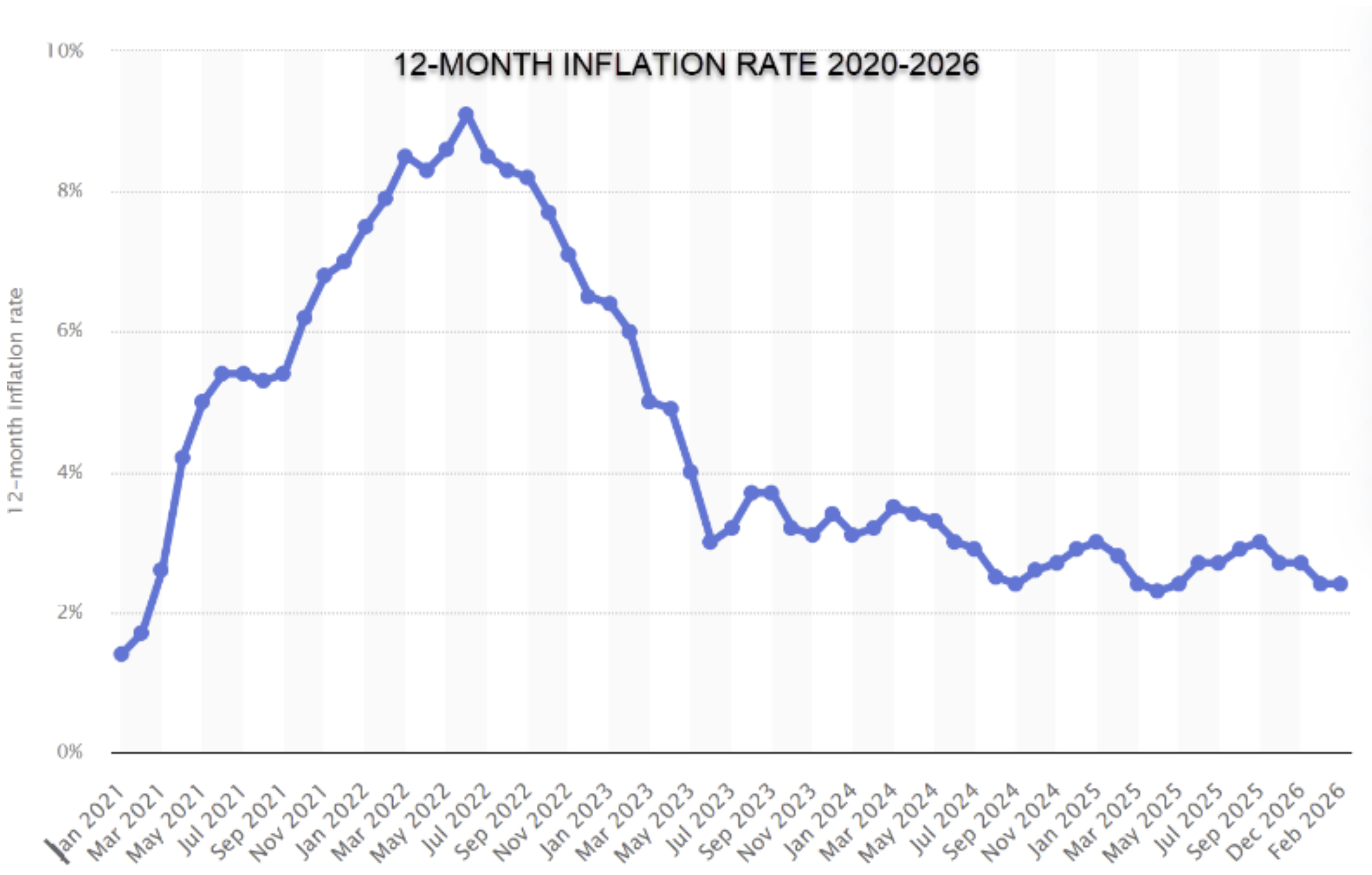

What we do know is that most of the economic policies—reduced immigration, tariffs, weaker US dollar tax cuts and spending growth, Fed Reserve rate cuts, and now global oil prices—are all inflationary. Unsurprisingly, inflation is stubbornly above the 2% target at ~2.7%. It’s the lowest rate since Covid but still substantially above where the Federal Reserve feels safe cutting rates and stoking growth. As such, inflation risk remains—one reason (of many) we like rent-producing investment property as an inflation hedge.

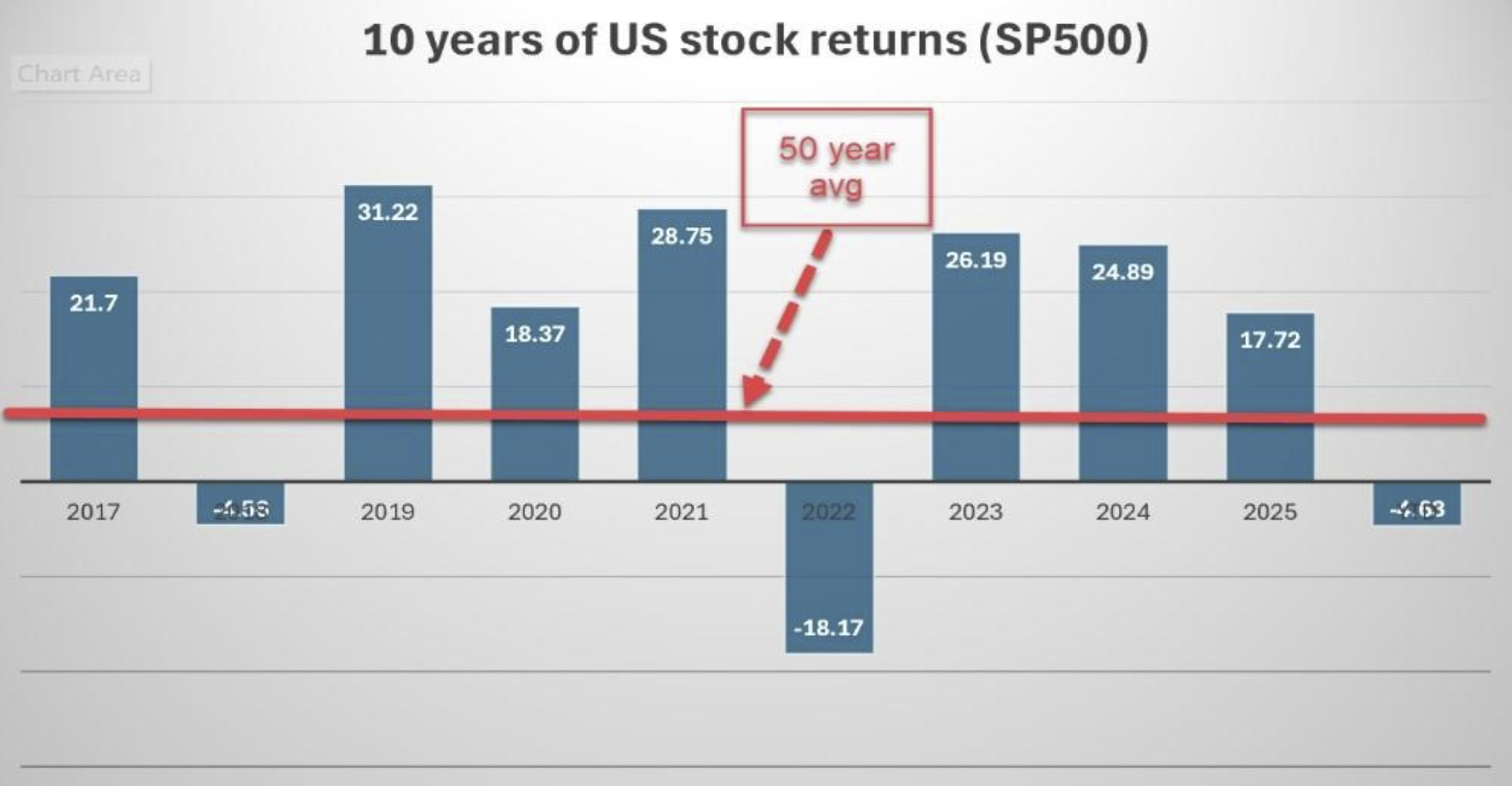

There is concern about a stock market bubble around Artificial Intelligence. Indeed, markets have gone up much more than their long-term averages (see graph). The most widely followed statistics on stock market valuations (Shiller 10-year PE) are nearing the dot-com era high. Artificial Intelligence stocks account for 75% of stock returns since the end of 2024. The top 10 companies, mostly AI-related, make up 40% of the entire US stock market—a higher percentage than ever before.

Will stocks crash and what do we do about that?

It’s not as immediately alarming as it might seem. Bubbles can go on for many years before they pop, and it’s usually worse to sell stocks, wait for the crash and time the recovery, which can take a very long time. Studies show concentration risk isn’t big, and from time to time things can get wacky. We have most of our clients positioned a bit conservatively, both in the asset allocation (ratio of stocks to bonds) and the stocks themselves are slightly defensive. The risk of market correction remains, but if you don’t need the money for the next 10 years, you should be fine.

International stocks and bonds outperform the USA

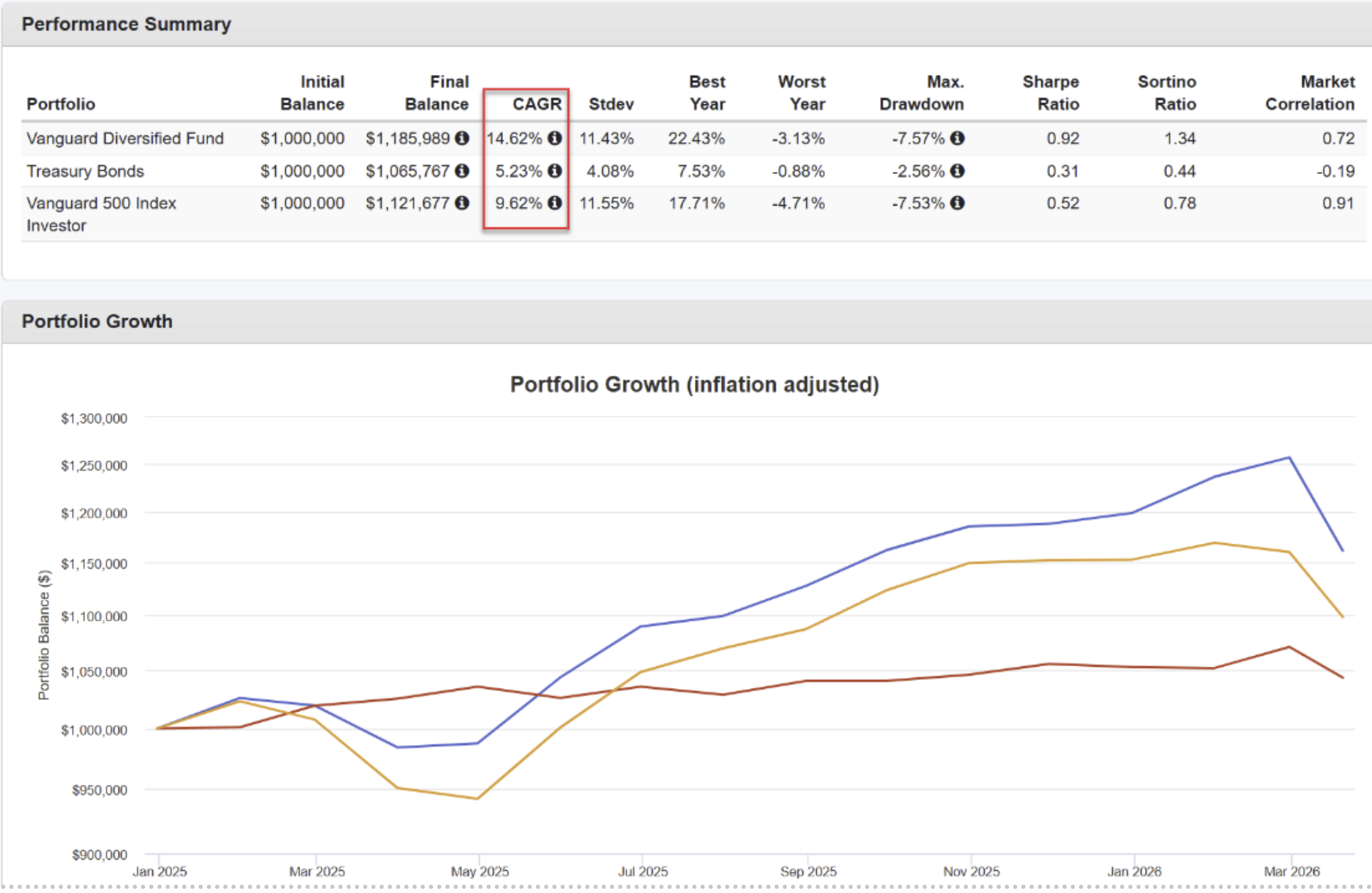

Perhaps the biggest effect has been the ‘debasement’ trade, or the reduced interest in investing in the US. This has caused US stocks, bonds, and currency to underperform the rest of the globe. The more you held of international and other non-US diversifications, the better your portfolio has performed recently. The diversified portfolio outperformed the S&P500 in 2025-2026 by 5% and continues to be the cornerstone of our investment strategy. (Look at the red outlined ‘CAGR’ pronounced ‘Cager’, which stands for ‘Compound Annual Growth Rate’).

Good news, earnings and unemployment

The two things that are incredibly strong are corporate earnings and unemployment. In the first dot-com bubble, highly-sought companies like Cisco, AOL, and Qualcomm had little or no earnings. Today’s AI giants are earning massive profits, and there are fewer overvalued start-ups. There is also steady employment. No, it’s not the same job market we (Gen X) had emerging from college, but there is paid work if you want in the medical, transportation, construction, and education fields. Consumer confidence remains lowish, but consumers continue to spend money.

Looking forward

As of March 27th, the S&P 500 has dropped 7% this year. This decline doesn't qualify as a ‘correction,’ which is typically defined as a market falling by 10%. A bear market occurs when the market has fallen by 20%. Corrections have happened in about two-thirds of years since 1928, making them quite common and not statistically unusual.